I have wanted to blog about this.

2019 is a year of major changes. This is the year I teach a big class of mix ability. I have always deployed myself to teach the weakest of all pupils, but my previous principal insisted that I change.

The challenges I faced teaching the class is small compared to the immense satisfaction I had as I see them grow and progress.

I am glad all of them pass with flying colors in PSLE. I had hope to produce at least 1 A*, and would have create history if I succeeded. Looking back, having pupils in my class fighting for an A* and believing that they could is already an achievement, because most came to me, just passing the subject. I remember the look in their face, when I told them they have nothing to lose, and everything to gain, if they fight for A*. No one will expect it from them, no one even talks about it with them. It is a high point in my teaching, when those who are already achieving A did not rest on their laurels and continue to push themselves.

This is also the year, I lost my dad. It was a painful year for him, as his health deteriorated. Care-giving could be tiring and frustrating at times. It is also a challenge trying to juggle work with care-giving. I remembered asking pupils to come back for extra lessons during the June holidays and my dad's conditions took a turn for a worse. I didn't cancel those lessons, and I am only 1 day into the week lesson when my dad passed away in the evening.

Strangely, the feeling of lost struck with me for a while, but the grief went away quite quickly.

I was getting ready to return to school when I suddenly had the symptoms of a heart attack. I went to A and E and was admitted to hospital for 3 days. Luckily, its a false alarm and the doctor said the cause could be due to the nerves at the neck being strained.

My health in 2019 was really bad. I had difficulties breathing and need to be put on inhaler. My annual health check also show red flags regarding the liver.

However, I was generally still grateful and happy for the year, as I prepare the biggest change in my worklife. I decided to step down as a HOD and prepare to be a senior teacher. The building up of the portfolio is quite painful as I hate report writing. The OPEN Class experience is also a painful one.

But as I wind down the year, I realize I am happier, looking forward to 2020.

However, perhaps because I grown so close to some of my pupils (I would think the feelings might not be mutual), I actually missed them, and I am quite surprise and sad that some did not come over to talk to me or say good bye during the day of results release.

Monday, November 25, 2019

Wednesday, November 20, 2019

Company prospecting: Kingsmen

Kingsmen stock price has tumbles. I shall not bored u with numbers and analysis other bloggers have blogged about. (Fifth person write up is good)

Nerf experince park is touted as one of the grow drivers for the company, and possibly to scale up to expand overseas or locally.

My scuttlebutt online from Google reviews is poor.

https://www.google.com/search?client=ms-android-xiaomi-rev1&sxsrf=ACYBGNS3C0Au2IMzHmuq3PEYEL96qM1uiw%3A1574068728343&ei=-GHSXaa1FOyZ4-EPvMSemAI&q=nerf+action+experience+review&oq=nerf+action&gs_l=mobile-gws-wiz-serp.1.1.0l8.1143.2031..3273...0.1..1.410.1320.2j1j3j0j1......0....1.........0i71j0i67j0i131.qqgQD2fwvVw#fpstate=uep_lurev_0x31da195490a33df3:0xea3d070414c5dafd

I ask my wife to bring my son, niece and nephew to visit the "playground". It is actually just that, with competition of SPARK at suntec which is within walking distance.

There is also bounce, concept or thematic playground.

None of the kids prefer Nerf over the other 2 experince.

I interview my wife and the kids in detailed. I think they make poor business sense. First, the place is small, and hardly crowded. (Granted it is a weekday, but hey, it's the holiday)

Second, out of 4 stations, only one is about shooting experience. There is a high element course, which I thought is common and can be seen anywhere. (U can find it at the zoo, not I am not kidding)

The unique experience of "compete" of shooting , need to be booked in advance and is fully booked when my wife and kids went over. Luckily the guide let them in for a quick game. Otherwise, there is totally no Nerf experince.

My kids prefer bounce at cinesleisure or spark at suntec.

My business sense is if nothing is changed for the experince, I have doubts over its survivability, nevermind profitability.

I had wanted to acquire Kingsmen as a possible turnaround play. Now, I passed.

Friday, November 1, 2019

Advertisement: Cakes for sale

Advertorial

A friend of mine is a freelance Baker of cakes. Her cakes are creative and can be customized to your needs.

https://www.facebook.com/cativatingcakeandcupcake/

Beautiful isn't it.

If u really interested, call her and say u are referred by Mr Ng, u will get a discount. Although this is advertorial post, I receive no referral incentive of whatever. Hahaha.

If u really interested, call her and say u are referred by Mr Ng, u will get a discount. Although this is advertorial post, I receive no referral incentive of whatever. Hahaha.

A friend of mine is a freelance Baker of cakes. Her cakes are creative and can be customized to your needs.

https://www.facebook.com/cativatingcakeandcupcake/

Beautiful isn't it.

Thursday, October 24, 2019

Random thoughts: A hot pan to another

Recently, I was considering a career move. Due to a recommendation by a friend, I explored a partnership in a potential venture.

The discussion didn't end well. I gave the matter some.thoughts and decided to talk to more people.

After that, I realised I might be jumping from one hot pan to another.

Made me feel better although nothing much has changed. I do not think I will continue that venture.

Another blogger made me realise there is a big difference being wanting to start your own business and wanting to be self-employed.

So... I decided to be manwhore one more time. Since now I have a different boss and going to have a different job scope next year.

I given up my chance for any future promotion or pay increment with this lateral movement to another job scope. But I am very happy.

Today, I finished my last appraisal work. No more. While I know there will be plenty of challenges in the future, I know I will be more at peace. Better to do what I am good at then trying to convince myself that I can do something I no longer believed in well

I really like the 3 questions Jack Ma asked himself. What do I have? What can I do to what I have? What I am willing to give up for what I have.

I know what I am not willing to give up just yet. So is time to shut down and be at peace.

I might still keep that option open and look it for various angles.

Here is a picture I find really interesting.

The grass is always greener at the other side; there is always a more shitty job.

Tuesday, October 22, 2019

Random thoughts: What my P6 kids want?

It's been 3 years since I start asking my P6 pupils to make name cards for themselves. I told them to think of what they like, and that the job they want need not exists in reality. I quoted past years examples like Pokémon Trainer and Hacker.

This year is really fun. The session is a good opportunity for me to talk to them about their interests.

This year, the choices are more varied and interesting. I have

1) Kept Man

2) Housewife ( Although I think they are referring to Tai Tai)

3) Gym manager

4) Gardener

5) Female pilot

6) Dancer

7) Game Streamer ( Something I learned)

8) Assassin

9) Ah long (She keep saying "legit one, legit one")

It is really fun talking to them. One very guiet girl designed a name card of a singer with a studio company. She looked up at me and suddenly start rapping, saying she wanted to be a star and that she think she can do it. I replied with a rap (cannot shu Sia)

The assassin wannebe name card is the design of death note.

I tease many of the pupils as they talk about their "dream"

Hope they remind innocent and dreamy. Is a hallmark of youth.

Thursday, October 17, 2019

Wednesday, October 16, 2019

Bragging rights: MIT

Warning: Irritating Post LOL

I have always had that elusive 2 baggers. It's like a badge of shame. Never holding something long enough due to lack of conviction or greed for a quick profits.

I am always jealous of CW 10 baggers hahahha, although not in a malicious way.

Finally, I got 1 2-baggers.

MIT!!! Yeah! I brought it in 2014 Dec at 1.45, including dividends receive over the last 4 years, and capital gains, I would make over 100% if I sold it now.

If u looking for reasons for this wonderful win, I will say luck.

Hahahah. Finally got lucky.

I already said this is a irritation post. Size too. It's not a big amount of my portfolio, so I just let it be and didn't have the intention to sell. Of course, my original thesis did not change and I did not really have to do hard review. I did want to add at 1.7 but it didn't reach the price after I did a review 2 years ago.

Yeah!

Wednesday, October 2, 2019

随心笔: 怪胎

怪胎吧。

忙完了,很空虚。

很想念,很舍不得,

却不知道说什么。

在身边的,不珍惜。

盲目地给,

不知道对方要不要。

怪了,也就一起走过十个月。

却常常觉得心缺了一块。

他们还在,好想跟他们多说几句。

但不知道说什么。

说出来的都是废话。

很可笑吧。

也许,有人希望我跟他们说废话。

但话却又少的可怜。

脑筋空出来了,

总是胡思乱想。

原来忙,是我的避风港。

现在,

突然会想起爸爸问我够不够钱花。

会看着手机,

有没有学生问问题,

有没有学生传口试录音。

现在,

在听另一个年级的口试录音。

好像在找替身一样。

替身的背后,还有去年他们的影子。

奇怪了。

我真是怪胎。

忙完了,很空虚。

很想念,很舍不得,

却不知道说什么。

在身边的,不珍惜。

盲目地给,

不知道对方要不要。

怪了,也就一起走过十个月。

却常常觉得心缺了一块。

他们还在,好想跟他们多说几句。

但不知道说什么。

说出来的都是废话。

很可笑吧。

也许,有人希望我跟他们说废话。

但话却又少的可怜。

脑筋空出来了,

总是胡思乱想。

原来忙,是我的避风港。

现在,

突然会想起爸爸问我够不够钱花。

会看着手机,

有没有学生问问题,

有没有学生传口试录音。

现在,

在听另一个年级的口试录音。

好像在找替身一样。

替身的背后,还有去年他们的影子。

奇怪了。

我真是怪胎。

Friday, August 2, 2019

随心笔:教书

十五年了。

一直都很拼,

希望学生会考得好。

每次考试时,自己都会很疲倦。

好像跑到终点的那种感觉。

这一年,又快结束了。

教毕业班,总是有心快缺了一块的感觉。

知道他们快离开了。

觉得很奇怪,好多都像成了朋友,

或者孩子。

在学习上,也许对他们比对我孩子用心多了。

我也有点内疚,

明明不是亲家人,

为什么不把更多精力放在自己孩子上。

反正一年后,大部分的学生也不会再见到了。

我觉得有点累,

有时,进课室,觉得很无趣。

最近常常骂学生,瞪他们。

教学法一直在跟新,我觉得我快跟不上了

我也不屑跟上。

这就是十五年的问题。

我傲了,老顽固了。

吃不到葡萄说葡萄酸了。

我心里对教学的疑惑,

没人问吗?

为什么这么重视一堂课怎么教,

我跟着理论走,为什么总是行不通。

我觉得好的办法,为什么总是让人觉得太简单?

这一年,我觉得很幸苦。

我觉得我是个好老师,

因为学生会来找我打篮球。

学生哭了,也会来找我 。

老师做到这样,不够吗?

但是好像这场仗越打越无胜算。

不知几时会满盘皆输。

我是否应该早点离开?

把还有仅剩的一些美好回忆带走。

Sunday, July 7, 2019

Company Prospecting: Modeling future earnings of companies

I have finished reading the book "Common Stocks, Common Sense", and have re-read a few chapters twice. I can really relate to the statement about modeling future earnings through qualitative analysis and "guessing" than just simply extrapolating pass data into future. This is especially true for companies that are cyclical in nature. It is not really meaningful to DCF its value, because the earning might be quite volatile. Reits might be a better target to DCF.

To cut the story short, I will like to share how I have applied my own future modeling using Singapore Companies as case studies. Readers who are interested, please read the book, as I am just trying to scratch the surface with my explanation.

First Step: Look for Market leader.

The reason is simple. I want a company that can captured the industry upturn. A company that will gain when industry turn around and not continue to be a laggard.

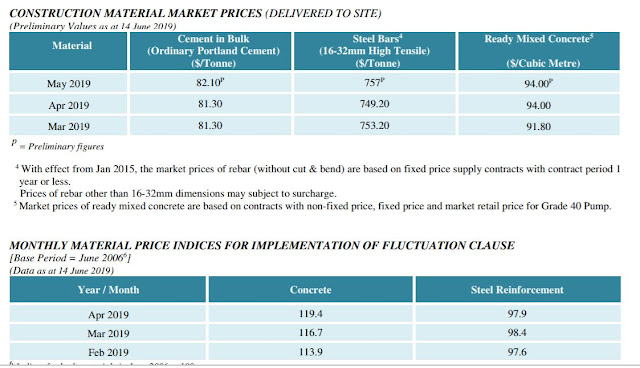

The example, I am using is PAN United. Looking at Revenue.

Pan United Rev from Cement and Construction materials

2018: 545,710,000

2017: 527,674,000

2016: 577,639,000

2015: 668,421,000

You can see from here there is some sort of correlation and according to https://brandongaille.com/18-singapore-cement-industry-statistics-and-trends/

PAn united is the biggest Cement supplier. Engro, another Cement Supplier listed Singapore managed

2018: 153 mio

2017: 141 mio

2016: 144 mio

So I think there is no doubt Pan United is a Key Market Player that will stand to gain when industry upturn happen.

Second Step: Check for correlation

Profits from the segment of construction material

2018: 8,496,000 with rev 545,710,000

2017: 8,958,000 with rev 527,674,000

2016: 10,657,000 with rev 577,639,000

2015: 12,859,000 with rev 668,421,000

2014: 24,219,000 with rev 612,097,000

2013: 39,406,000 with rev 599,049,000

You can see margin destroyed due to lower demand as well as competition. But Pan United has hold market share reasonable well.

One more chart.

You can see the "good times" correlate to good price of cement RMC.

I am aware of different grade of RMC, the one included in BCA statistic is Grade 40, and there are different type of Concrete, some quick solidifying, some green and carbon neutral, but I still think is a reasonable calculated guess.

So is 2016 - 2018 horrible years in construction demand? From BCA data, the demand for construction in those three years are:

(Data from BCA)

2018 - 27 bio

2017 - 24.5 bio

2016 - 26.1 bio

2015 - 27.2 bio

2014 - 37 bio

Again, it seem 2014 is the golden year for a good reason.

BCA projection of demand is always announced in January. In January the projection is

RMC price is better in Q2 than in Q1, and Pan United Q1 results is already better in 2019, than 2018. I assume that the worst is over for Pan United.

In the book, the author model precise earnings.

I will pass giving a giving an exact figure, I will instead guess a range of possible earnings. Assuming if price of RMC return to the good old days of 110 and above, will margin be closer to the bountiful of years of above 5% ( >6% in 2014)?

2018 margin is at 1.5%, it does not need a party for margin to double. Assume Status Rev 550 mio in 2019 and 600 mio in 2020 (Where the demand for the IR should start flowing), and Margin of 1.8% in 2019 and 2% in 2020, we should see profits of 9.9 mio and 12 mio.

Even if margin double, the best case and most optimistic scenario, it is still only half of what it is like in the good old years. So for a conservative projection, we see EPS of about 1.4 cents, 1.66 cents in 2020.

Assuming pay out ration of 80%, dividend will 1.12 cents and 1.32 cents.

So at current price, PE for 2019 can be 24 times or at good as 12 times (If margin improve to 3%)

Yield can be 3% or 6%

So at current price, it makes no sense for me to add, no matter how much I like it. I bought my first tranche of Pan United at 28.5 cents, so valuation use, it makes slighly more sense at future PE of 20 times or 10 times, and dividend of near 4% to 8%

As I mention earlier, I did a range of valuation than giving a fix figure, but if second quarter earnings makes 1H earning out of my expected range of earning, I know it is time to say good bye.

.................................................................................................................................................

This is the first time, I spent so much time writing an article on investment, I will leave QAF modeling to next time. (Not vested in QAF)

To cut the story short, I will like to share how I have applied my own future modeling using Singapore Companies as case studies. Readers who are interested, please read the book, as I am just trying to scratch the surface with my explanation.

First Step: Look for Market leader.

The reason is simple. I want a company that can captured the industry upturn. A company that will gain when industry turn around and not continue to be a laggard.

The example, I am using is PAN United. Looking at Revenue.

Pan United Rev from Cement and Construction materials

2018: 545,710,000

2017: 527,674,000

2016: 577,639,000

2015: 668,421,000

You can see from here there is some sort of correlation and according to https://brandongaille.com/18-singapore-cement-industry-statistics-and-trends/

PAn united is the biggest Cement supplier. Engro, another Cement Supplier listed Singapore managed

2018: 153 mio

2017: 141 mio

2016: 144 mio

So I think there is no doubt Pan United is a Key Market Player that will stand to gain when industry upturn happen.

Second Step: Check for correlation

Profits from the segment of construction material

2018: 8,496,000 with rev 545,710,000

2017: 8,958,000 with rev 527,674,000

2016: 10,657,000 with rev 577,639,000

2015: 12,859,000 with rev 668,421,000

2014: 24,219,000 with rev 612,097,000

2013: 39,406,000 with rev 599,049,000

You can see margin destroyed due to lower demand as well as competition. But Pan United has hold market share reasonable well.

One more chart.

You can see the "good times" correlate to good price of cement RMC.

I am aware of different grade of RMC, the one included in BCA statistic is Grade 40, and there are different type of Concrete, some quick solidifying, some green and carbon neutral, but I still think is a reasonable calculated guess.

So is 2016 - 2018 horrible years in construction demand? From BCA data, the demand for construction in those three years are:

(Data from BCA)

2018 - 27 bio

2017 - 24.5 bio

2016 - 26.1 bio

2015 - 27.2 bio

2014 - 37 bio

Again, it seem 2014 is the golden year for a good reason.

BCA projection of demand is always announced in January. In January the projection is

Third: Guess Industry upturn

It seem it is going to be a slow year yet again, but the 9 bio expansion by MBS and Genting are announced in April, and I am quite sure assuming 3 Bio A year over the next 2 years when construction start, this demand is not captured in the projection, at least not accounted for in the lower end of projection

Worst case scenario, up to April, it is on track to hit the lowest 27 Bio Demand, so it should not get any worse. Reading on Pan United Quarter reports and BCA announcement of big tenders, various En-Bloc redevelopment again seem un-captured in 2018.

RMC price is better in Q2 than in Q1, and Pan United Q1 results is already better in 2019, than 2018. I assume that the worst is over for Pan United.

In the book, the author model precise earnings.

I will pass giving a giving an exact figure, I will instead guess a range of possible earnings. Assuming if price of RMC return to the good old days of 110 and above, will margin be closer to the bountiful of years of above 5% ( >6% in 2014)?

2018 margin is at 1.5%, it does not need a party for margin to double. Assume Status Rev 550 mio in 2019 and 600 mio in 2020 (Where the demand for the IR should start flowing), and Margin of 1.8% in 2019 and 2% in 2020, we should see profits of 9.9 mio and 12 mio.

Even if margin double, the best case and most optimistic scenario, it is still only half of what it is like in the good old years. So for a conservative projection, we see EPS of about 1.4 cents, 1.66 cents in 2020.

Assuming pay out ration of 80%, dividend will 1.12 cents and 1.32 cents.

So at current price, PE for 2019 can be 24 times or at good as 12 times (If margin improve to 3%)

Yield can be 3% or 6%

So at current price, it makes no sense for me to add, no matter how much I like it. I bought my first tranche of Pan United at 28.5 cents, so valuation use, it makes slighly more sense at future PE of 20 times or 10 times, and dividend of near 4% to 8%

As I mention earlier, I did a range of valuation than giving a fix figure, but if second quarter earnings makes 1H earning out of my expected range of earning, I know it is time to say good bye.

.................................................................................................................................................

This is the first time, I spent so much time writing an article on investment, I will leave QAF modeling to next time. (Not vested in QAF)

Sunday, June 16, 2019

Random thoughts: Book recommendation

Check out this book. I have really enjoyed it. An investment theme book.

Sunday, June 9, 2019

Company prospecting: Pan United

A very short write up. More for discussion and putting it on investment bloggers radar, than throwing in numbers.

Pan United is a leading supplier of cement in Singapore. Hence their business depends on the demand of the construction sector. Information from BCA show that demand is picking up. The lowest projection of demand is expected to go up over the next few years. The projection came before the announcement of IR expansion. I am not sure if the 9 billion investment is accounted for, I assume that even if it is accounted for, all these would mean the projection Should come to the mid range of projection of close to 30 bio.

When the construction sector is declining in Singapore, pan United still manage to increase revenue and hence improve market shares except for the last 2 years.

Pan United is a leading supplier of cement in Singapore. Hence their business depends on the demand of the construction sector. Information from BCA show that demand is picking up. The lowest projection of demand is expected to go up over the next few years. The projection came before the announcement of IR expansion. I am not sure if the 9 billion investment is accounted for, I assume that even if it is accounted for, all these would mean the projection Should come to the mid range of projection of close to 30 bio.

When the construction sector is declining in Singapore, pan United still manage to increase revenue and hence improve market shares except for the last 2 years.

If u do some tracking, at its Peak of it profitability, Revenue is half of what it is now but net profits is double of what it is now. Margin keep getting squeeze and became.lower and lower. RMC prices has shown some recovery ij the recent quarter but nowhere near its peak. If u look at Q1 reaults, it has double its profits simply by improved margins and RMC price ccontinue to improve due to expected higher demand in construction.

Beside the IR, the Deluxe of En bloc demand seem not BEING captured in 2018 as the BCA projection was higher than the actual Billings. So I am rather confident that construction demand will be nearer to 30 bio this year (clearing of backlog of developnent of En bloc site) and beyond in 2020.

Pan united has maintain profitability when demand hover around 26 to 29 bio.

Construction is turning, and I expect earnings to double.

Hence there is a chance for a yield play plus capital apprecitation to happen if pan united does double its NP for 2019.

Vested and maiden investment made at 28.5 cents. DYOD.

IF anyone has this in your radar, please leave a comment and I would really like a discussion.

Thursday, June 6, 2019

随心笔:祭父文

首先,谢谢各位到这里,陪我和家人送父亲走这最后一程。我代表大姐大哥,表示感激。

我父亲是一个对生活充满热忱又独立的人。记得他常常对我说,担心自己不能走动,那样就遭了。

记得有一回,他跌倒到了。肋骨有点微裂,医生说要吃止痛药,但他却说不是很疼。他在我眼里,他很坚强。

后来,即使需要使用拐杖助走,他也事事亲历亲为。我知道在医院的那几个月,他很辛苦,因为不怎么能下床。他时不时会问我,几时能回家。

最后在家的几个月,当他痒得呻吟,痛得叫出来时,我知道,他很辛苦。当姐姐对我说,他笑着离开,很安详,我虽然有点难过,但是还是很感恩,他的苦难结束了。爸爸,接下来你放心,一路好走。

在我眼里,我爸爸不善表达爱。他从来没说过我爱你,记忆中好像至我懂事也没抱过我。但是,我知道,也感受到你的爱。

以前我服役周末回家,你会帮我盖被。其实我容易醒,也怕热,但是很喜欢你帮我盖被的感觉。

后来,我念大学时,周末会去餐厅打工。值夜班回来,他对会叫我喝鸡精,说睡这么少应该会很累。

我每次给你家用,你对会问我自己够不够用,还会常常叫我给少一点。爸,你放心,我虽然非大富大贵,但还是遗传了你的那么一点点傲骨。我不怕吃苦,在新加坡只要肯努力,生活不会过不去。你靠着两只手,和妈妈煮了二十几年虾面,养大我们,你没受教育,却让我从你身上学到了不少道理。

爸爸,我们姐弟三人也爱你。虽然我也从没说过,但是我相信你也会感受到。以后不能再带你去吃晚餐了。我会想念你。

Friday, May 17, 2019

Coporate updates of Silly InC

Dear readers, Silly Inc has sold all it netlink shares and make its maiden investment into capitaland.

Netlink has play out mostly as the board wanted. Dividends increase, growth in profits, etc. However, the growth is too slow to offset the 45 mio in loans that are used in distributions.

The board would be more hopeful had the growth be more impressive. Going forward, Capex will.most likely increase and if the rate of growth is to continue, netlink could, at best, offset the 45 mio in distribution but they could hardly increase dividends anymore without either CONTINUING WITH THE LOANS DISBURSEMENT OR INCREASE LOANS TO DISBURSE as dividends.

APPT is a good lesson and reference. While the 2 companies are different with different growth sectors and Netlink seem more likely and also competent to capture the growth, it is never a great idea to use loans for distributions.

What happen if Netlink do not use loans anymore? The fall in shares price could be drastic. But Netlink won't do it, they are not stupid. They have enough debt room and cash flow to be on morphim for a long time and hope for growth to come to the rescue.

However, enjoying a 6 pecent yield while facing with such risk seem illogicial. Silly inc had APPT for 11percent yield and manage to offload it for capital gains yeARS ago. The riSK reward profile do not seem attractive.

With the increase in cash, there are several potential companies that silly inc would like to accumulate at the right price.

The company bought Capitaland not based on ratios but the fact that many did not realise the Capitaland will be a very different animal after the merger.

First, there will be a significant ARA type of fund management business. There are many ways to cash in the cow. Put all the reits under one managemENT and IPO it.

Offload different assets to different reits to recyle capital.

Last but not least, it will be able to truly build a whole township without the need to subcontract. Vietnam is industrial towns hot bed, capitaland can build hotels, malls, factories and homes, and also manage it, and sell it for any governmemt overseas.

Capitaland is not a value or turnaround play, but is a good concept play, and the possibities to cash in after the merger is quite aplenty, and those coporate actions make good story headlines.

Netlink has play out mostly as the board wanted. Dividends increase, growth in profits, etc. However, the growth is too slow to offset the 45 mio in loans that are used in distributions.

The board would be more hopeful had the growth be more impressive. Going forward, Capex will.most likely increase and if the rate of growth is to continue, netlink could, at best, offset the 45 mio in distribution but they could hardly increase dividends anymore without either CONTINUING WITH THE LOANS DISBURSEMENT OR INCREASE LOANS TO DISBURSE as dividends.

APPT is a good lesson and reference. While the 2 companies are different with different growth sectors and Netlink seem more likely and also competent to capture the growth, it is never a great idea to use loans for distributions.

What happen if Netlink do not use loans anymore? The fall in shares price could be drastic. But Netlink won't do it, they are not stupid. They have enough debt room and cash flow to be on morphim for a long time and hope for growth to come to the rescue.

However, enjoying a 6 pecent yield while facing with such risk seem illogicial. Silly inc had APPT for 11percent yield and manage to offload it for capital gains yeARS ago. The riSK reward profile do not seem attractive.

With the increase in cash, there are several potential companies that silly inc would like to accumulate at the right price.

The company bought Capitaland not based on ratios but the fact that many did not realise the Capitaland will be a very different animal after the merger.

First, there will be a significant ARA type of fund management business. There are many ways to cash in the cow. Put all the reits under one managemENT and IPO it.

Offload different assets to different reits to recyle capital.

Last but not least, it will be able to truly build a whole township without the need to subcontract. Vietnam is industrial towns hot bed, capitaland can build hotels, malls, factories and homes, and also manage it, and sell it for any governmemt overseas.

Capitaland is not a value or turnaround play, but is a good concept play, and the possibities to cash in after the merger is quite aplenty, and those coporate actions make good story headlines.

As for the recent headlines grabbers on tradewar etc. The company is in the view that all investments should take into considerations the downturn of market. We hold a considerable amount of cash, close to 50 percent, as risk management. There also other funds like CPF OA and SRS that are hardly utilize as of now.

So silly Inc will just continue to do the silly thing of prospecting companies with growth prospects and wait for the right price instead of worrying of trade war or otherwise as a market correction and a gentle bear is already planned for in company cause of action. The company do fear a prolong Winter Bear as company has no experince with it.

There are already a few counters close to purchase price and silly Inc has made a few bids with no avail. Silly Inc will.update as and when there are deals made.

Silly Inc would.like to assure interested readers that it will continue to be prudent and would like to share The portfolio excluding cash is still doing well, with only 2 counters trading below cost

Saturday, May 4, 2019

SillyInc corporate update : First Reit Accumulation

Silly Inc recently double the holdings of FR in portfolio. The Average price is 97 cents including costs.

The board is in the view that default risk by Lippo K (Biggest rental income customer 87%) is non-existence, since the rights exercise by Lippo K (yet to materialize)

However, since then, First Reit has been falling from above $1 to the low of 93 cents recently. All the known risks have been reduced, yet FR fall instead of rise.

Lets visit the risks:

1) Execution of Meikarta Project by Lippo K (Top management did not get indicted, and there is no adverse updates since then)

2) Default Risk (Almost non existence now, if they raise the fund like they say they would. 1 billion would have wiped off all the loans the parents company had, but of course, 200 mio will be earmarked to develop Meikarta

3) 2021 lease renegotiation to be in Indonesia Currency instead of Singaporean dollars. Well, it will expose one to currency risk indeed.

4) Asset dumping by OUELH or Lippo K. The troublesome and lawsuit laden China projects from OUELH cannot be dumped due to the litigation going on. Japanese home is likely dumping candidate. Hence this post is to provide some numbers for this high probable dumping.

Now the Maths:

Japan homes asset = 290 mio

Yield = 5.5 %

Rental revenue = 16.7 mio

Assumption: (All scenario based on market price of $1, the cheaper u get in, the better the deal)

1) 90 mio by debt, 200 mio rights/ placement (discount at 90 cents)

Future yield becomes 7.6%

2) All Debt. Yield accretive. 9%

3) All rights. Yield 6.9%

4) 140 mio debt (Almost Half), Yield 8%

Board in the view that all rights or all debts way to acquire Japanese Homes is unlikely.

So we are looking at yield at 7% upwards, asssuming they dun price too large a discount, and issue shares at below 90 cents.

Company did not calculate till 2 decimal place and readers are to do due dilligence. Company will most probably trade this counter and will monitor it closely with profit taking and loss cutting markers.

The board is in the view that default risk by Lippo K (Biggest rental income customer 87%) is non-existence, since the rights exercise by Lippo K (yet to materialize)

However, since then, First Reit has been falling from above $1 to the low of 93 cents recently. All the known risks have been reduced, yet FR fall instead of rise.

Lets visit the risks:

1) Execution of Meikarta Project by Lippo K (Top management did not get indicted, and there is no adverse updates since then)

2) Default Risk (Almost non existence now, if they raise the fund like they say they would. 1 billion would have wiped off all the loans the parents company had, but of course, 200 mio will be earmarked to develop Meikarta

3) 2021 lease renegotiation to be in Indonesia Currency instead of Singaporean dollars. Well, it will expose one to currency risk indeed.

4) Asset dumping by OUELH or Lippo K. The troublesome and lawsuit laden China projects from OUELH cannot be dumped due to the litigation going on. Japanese home is likely dumping candidate. Hence this post is to provide some numbers for this high probable dumping.

Now the Maths:

Japan homes asset = 290 mio

Yield = 5.5 %

Rental revenue = 16.7 mio

Assumption: (All scenario based on market price of $1, the cheaper u get in, the better the deal)

1) 90 mio by debt, 200 mio rights/ placement (discount at 90 cents)

Future yield becomes 7.6%

2) All Debt. Yield accretive. 9%

3) All rights. Yield 6.9%

4) 140 mio debt (Almost Half), Yield 8%

Board in the view that all rights or all debts way to acquire Japanese Homes is unlikely.

So we are looking at yield at 7% upwards, asssuming they dun price too large a discount, and issue shares at below 90 cents.

Company did not calculate till 2 decimal place and readers are to do due dilligence. Company will most probably trade this counter and will monitor it closely with profit taking and loss cutting markers.

Thursday, April 25, 2019

Random thoughts:

Had been a few hectIc weeks.

However, I still offered to help train the volleyball teams every morning. I really enjoyed the sessions. I feel that the teacher IC is helping me more than I am helping her.

Today, the senior boys team became the national champions. A proud moment for them. There will be no more morning trainings, and I think I am really going to miss them.

At age 40, the last 4 weeks is really God send. I felt I went back to my secondary school days. My school is a notorious school, but I have very fond memories of my CCA trainings.

The jumping and spiking hurt my ankle and knee. I need those guards now. I am no longer young, and the joints hurt. But I really miss those sessions, in fact, I am feeling rather down now.

Those days. Eh... training everyday. My team mates, our friendship.

Will I choose another secondary school? No.

Monday, April 15, 2019

随心笔:无思

有时真的不知道自己在做什么。

好像就随波逐流。

也不清楚自己的努力,是不是白费的。

更不清楚自己是不是在自欺欺人。

但是天还是要亮,

路还是要走。

就一步一步走下去吧

希望是柳暗花明又一村,

而不是跌入万丈悬崖。

或许,悬崖下,是清碧潭水。

脚步停一停,听一听。

不要太在意,

周围的环境,

不要太理会,

前方的路。

认定了目标,

走了冤枉路,

绕过来就是。

Friday, April 5, 2019

随心笔:回家

回家了,终于。

不管好坏,不论结果。

家,就算什么也没有。

就算能做的事,也没差。

我还是希望,

还是开心。

那个药箱,不会再空着了。

你不一样了。

你听不太懂我的话。

你要想一想,才记得我的名。

没关系。这是你的地方。

你安心休息。

你越来越像小孩。

你其实不再是你了。

你好好休息,开心一点。

希望能带你去吃点饭。

Thursday, April 4, 2019

随心笔:失去

不是离开了,才会失去。

握在手中,也不一定拥有。

不是活着,就是存在。

没有抓不抓得住,

只有做着想做的事。

失去,好好活在当下吧。

没有拥有,就不会失去是屁话。

好好拥有,活在心里。

眼前的,让他去吧

Random thoughts: Old age and money

Its less than 3 years apart since my mun passed away and there is a need of active givegiving for my dad.

I am closer to my dad. Hence, the last 3 months sometime do send my mind to a roller coaster ride.

There is a period of time, I worried for my single child. I thought of checking myself in to a community hospital or home and paying the expenses from my rental. There is no need for my son to worry about me falling, etc.

Having been to the hospital for 3 months. I know how it feels to be staying a hospital, community or otherwise. I rather die at home and is glad that my dad is finally going to be discharged. If lying on the bed 24 hours and wearing pampers is distressing enough, I would not want to stare at the fellow patients, each with different ailments.

I wonder how it would be when my tine comes.

Its a humbling experince. I think I do hope to see my son trying to make me confortable, and talk to me, when it is my turn.

Money, is really not at the back of my mind.

Anyway, talking about money. Do look around construction companies and construction supply companies. rWS and MBs spending 9 billions. Assume construction takes place over 3 years, and annual demand of construction in Singapore is in the range of |28 billion to 32 billion. Its 10 percent more, at the backdrop of continous govt spending on MRT lines.

Pan united is a big player in cement, and while MBS or RWS might use their own construction companies or overseas companies. No one is reallg going to ship cement from overseas.

Bye.

Wednesday, March 27, 2019

Random thoughts: be mindful of seeing the full picture.

Recently, I saw a lot of sponsored ads related to investment in Facebook. Some of my friends like the pages. Out of morbid curiosity, I look at the comment section of a online earning workshop that I know is just ......

I am surprised by the sheer number of people interested.

I hope with this post, people understand that I do not need to lie to mislead u. Just not telling you the full picture is enough.

I shall be upfront that portfolio returns (realised including dividends) or ROA for the last 3 years are 4 percent, 6 percent, 3 percent. Hardly beating any index or doing any better than CPF SA

Let me give examples that how without lying, I can mislead u that I do have a winning strategy.

For example,

"Learn how to identify turnaround companies and do cyclical plays. Get returns of 30 to 50 percent within just a year or two or even months. Learn how by analysis of industry trends, company competitive edges allow SI to buy Venture, ST enginnering, Silverlake Axis, Yangzijiang near their low and profit immensely"

I did not lie about the above statement. What I did not tell u is I sold too early, and missed mutibaggers if i have sold them later.

"How to buy at a low of 40 cent and see silverlake balloon almost 50 percent within a few months. Learn how to read fianancial results and identified trends of imminent upturns"

I didn't lie about the above statement too. What I didn't tell u is my average price of purchase is Not 40 cents but 47.5 cents. Suddenly the returns isn't too sexy.

I also didn't tell u I got SIA ENGINEERING turnaround wrong. I also brought Sarine Tech at av. Price of 46 cents and sold it 40 cents to cut loss, only to see it fell to 36 cents and then rebound to above my purchase price.

”learn how to invest in industrial REIT And enjoy CAGR in excess of 10 percent every year for the last 5 years"

I also didn't tell u I calculate capital gains but I have no intention of selling so there is no way to unlock the value. I also didn't tell u I only have 2 lots of Ascendas REIT so it is not going to make a big difference to my overall portfolio returns.

I am quite sure I am not reaching the intended right audience with my post but it satisfies my desire to brag about nothingness and delusuonally still think that it is worthy cause for a post

The good question to ask is how your portfolio is doing as a whole and how long have your been keeping to this portfolio.

Wednesday, March 20, 2019

Random thoughts: Midlife crisis part 2

This post is kind of triggered by B post and also Rolf about success.

While many congratulate him for able to resign, I think he is venturing out with something in a mind and is not exactly on FIRE.

I have been contemplating and researching on a possible plan where I strike it out on my own. I dropped hints to my wife and told her my intentions. While she has her reservations, she supported me if I do take the plunge. I really appreciate it.

We have convsersations, and she offer many other options and advices. I told her my plan is not so.much to escape and make a living and I agreed that there are much safer and less risky options (financially), rather I would like to build something.

Jack ma mention in one of his speeches that we should take risks when we are in the 30s, when we are in the 40s, do what we are good at.

I have calculatEd that I might have to eat grass for 2 years,and if things eventually dun work out, I would have wipe out my savings. I intend to use my investment portfolio for my undertaking.

SMOL poked we want out because we are losing the office politics. While I might not be winning, I hardly think surviving well will be a problem for me, especially after I make some plans to move aside.

It is really the crisis of seeing purpose in the work we do. I am rather delusioned with a lot of things the way they are.

I know I need to learn on the go and be willing to accept possible consequences from failures of my ventures.

However, there is still a part of teaching that I really enjoyed. The interaction with pupils, the bonds and relationships. Of course they are pupils I couldn't reach or couldn't stand me, but I overall, it is really fun.

At 40, I really appreciate every game of sport I still do with kids. I couldn't find adults to play with me, or maybe I didn't lIke playing with adults?

At the back of my mind, I have this thought, this could well be my last time I do this. I did some crazy things that I thought I would not do yeaes ago. Such as accepting invivtation to whatsapp groups and basketball game etc.

My conversation with them have also shifted from giving advices to bordering of talking nonsense.

Make me wondered one early morning, should I just shut up (Not just verbally but also cognitively) and just take my good pay (by my own standard) and just work with the kids and forget about the meaningfulness of othee part of my work.

From my investing style, I know I am a rather risk adverse investor anyway.

Friday, March 15, 2019

Random thoughts: The 3 little joys from teaching

Let me start by being me, cynical. I don't change lives, kids change lives on their own,because of circumstances or will. I just hope I am part of the positive influence in those circumstances.

So the joys I derived are from the small stuff. I however know of real flesh and blood people who stories are like those u see on advertisement.

So here goes.

1) when pupils understand the lesson and overcome a particular fear of learning.

When pupils finally understood the thinking process behind a language task, be it reading comprehension, or writing, they no longer need answers. They know how to get answers, nevermind that the answers may not be perfect. When they know they can apply it across different exercises, confidence is built.

The lesson where there is sparkle in the eyes, is just the begining. The famous 10K hours of practice for mastery hold true. Depending on the pupils competence, no one need 10K and no one has 10k hours, but if someone tell u there is no need for drill and practice, tell him to invest successfully after reading 2 books.

I remembered vividly that pupil who could not speak. She could memorise and prepare the work in advance. When ask to answer inprompt questions, she will panic.

I remember drilling her word by word, day after day, everyday. Advising her what could be said, how to say it, what are the common topics.

When she came up excitedly after her PSLE paper, telling me she could manage the questions, I knew she has a high chance of passing. I almost gave up. A year has passed when she wouldn't even open her mouth to utter a full sentence.

I knew she wanted to do well very badly and is trying very hard, so we all buckle down and do it, literally word by word, sentence by sentence.

That was last year batch. I think it also brought out the fighter in me. I remember going to my pupils word by word, having them do spelling by the strokes of their fingers 3 times a day. Going through the common words required for writing.

Words like ”thank you", "should", they couldn't write, but we just keep practising. In the morning before school starts, during recess, after school. Walking along the corridor and practising, countless make up lessons, just so that I can reach as many as possible my 10 weakest pupils.

I know many still frown on such drill and practices. I just have this to say. They are under my care to learn, and I teach. They need a score to go secondary and I make sure they work hard to get it, I am not dogmatic about ideals and is unapogetic about drilling.

Perhaps over drilling kill the joy of learNing for high achievers. But when u teach the weaker pupils, u are telling them u have not given up on them

2) When pupils enjoy learning.

I hope pupils enjoy coming to my class. But if I have to do 1) at the expense of 2) and will do it.

I like my class to be filled with laughters.

Problem is, I just have that much tricks, old tricks no longer funny.

But the younger ones usually more easily entertained.

3) When pupils share with me their personal problems

It is only this year, that pupils share with me their problems. Their social problems with friends (although the underlying cause is more than that hahahaha)

How their friends are talking behind their backs, spreading rumors and how they felt affected.

They say they want me to help or advice. But They dun want me to punish or scold their friends.

I am not too sure I am doing a great job advising. Hahahah. But when pupils came over and asked "Mr Ng, can I talk to u for a while", I felt trusted.

And wow, after listening to them, the kids' world are so happening! I can write a Korean drama with jealousy, betrayal, threats, spying, social traps... with adaptation.

My world even as as lower secondary teenager wasn't so happening.

Thinking back, after 13 years of teaching, that I have pupils willing to tell me their problem or sharing their frustration, I am not too sure if I have been missing something in the last 13 years.

Friday, March 8, 2019

Random thoughts: Just some musings

Caught myself ...

I realise I need a lot of affirmations in my work. Pupils' feedback, parents' appreciation, peers or bosses' praises.

In the earlier part of my career, I had a very nuturing boss, I was the golden boy at work, I had all of them above in abundance. Looking back objectively, I am sure I dun really deserve all those.

Perhaps, I am used to it. So when I am transferred to another school, the sudden cold turkey treatment gave me a shock.

Today, I realise all these affirmations depend a lot on the giver as much as the receivers.

Its not rocket science, but looking back, I receive affirmations and appreciations from parents who are generous with them, and are not struggling with work. I mean everyone struggle at work, but I meant those who literally faced some hardship. They already struggle to care for themselves and their charge, how can I expect affirmation from them. It should be the other way round, Me assuring them that their child will progress fine.

How about kids. In my previous school, due to their upbringing, kids are a lot more articulate.

I realISE as a child, I do appreciate a lot of teachers but I never show it.

Work, I have a quiet confidence of where I stand now. I know I am somewhere in the middle of the spectrum. Peers and boss recognition are no longer that important. Just likeminded workerS are all that is needed.

This article, is a reminder for myself, to stop looking for affirmation, although I realise I crave a lot for it. LOL.

For those who are helping others and dun feel appreciated. They know, u know, god knows, words are cheap, continue with your good deeds.

Tuesday, March 5, 2019

Random Story: Renewable Kinetic Energy

Has been a while... since I write a story, here goes...

----------------------------------------------------------------------------------------------------------------

In the year 4023, Earth is obsessed with Green Energy, and all its citizens globally are ruled with Iron hand. Not much is left, and hence the recovery process of earth start in Ernest in about 200 years ago. No one really remembered how life is like without the computerized instructions that are downloaded to our brains and humans simply obey for the greater good of Earth.

All humans aged 6 to 60 are required to run at least 40 kilometers a day, before they can get on to their daily routine. The running on the surf board create the clean kinetic energy needed to run the system. It is the closest thing to 100% zero carbon footprint energy.

When this programme started, of course, not many can run 40 km. Many refused to run, some tried their best and dropout. For those who could, they are not running as fast as they should. The energy generated is sub-optimal, and injury cases are common. Motivation is low, and the programme almost get scrapped because human resistance to this programmed instructions is high and many, regardless whether they are able to complete the race or not.

Hence, the programme start giving incentives to those who can run faster. Those who could not run, but walk the whole distance are also given some credits. Energy harvest improved. To improved the programme, all humans are classified as "Sprinters", "Runners" and "Walkers". Dropout almost become unheard of.

The programme was a great success. Sprinters not only run to complete the distance, they typically all tried to go for the finishing line fast, with 3-4 folds amount of kinetic energy produced that it otherwise would be. The top 1% pupils were given even more incentives and training were provided so that they can even run faster.

The runners also show 100% increased in productivity at least. Strangely, most injury cases now seem to stem from the runners and sprinters group instead of walkers.

To further increase the collective energy generated by all 3 groups. Sprinters are given the best time slot to run, and the most efficient surf boards to tap their energy. They will be the first to run, and only when they have almost complete their race will the runners start, followed by the walkers.

Over time, Walkers are call Slackers. Slackers also felt that they could never be runners.

There are opportunities for Walkers to be promoted to the tier of Runners or even Sprinters, by such cases are few, and they usually take place at a much older age.

Energy harvest was at its peak.

Until one day...

The energy harvest seem to repel each other. The bulk of energy harvest from walkers seem to repel the energy from sprinters. While sprinters produced plenty of energy, the bulk of the human populace are walkers, and their energy output is not to be scoff at. The "pure" energy of Sprinters could not blend well with the energy of walkers.

Efficiency worsen and the blame game start.

It took 10 years before research show that the brains perception and thoughts during the run affect the nature of the energy produced.

So now, there is no more sprinters, runners and walkers. All of them run together, and there are different group in different permutations. Some times, all sprinters are still group together, but most groups would consist at least of runners. Walkers now start the journey together with runners and sprinters. It is hoped that there is more positive energy generated net, and walkers will have more motivations and opportunities to increase speed of running. Sprinters will have less injury cases and will slow down when necessary. There are still explorations of the right permutation to generate maximum harmonious energy

-----------------------------------------------------

Ok... Its not a story actually... Hahaha

Monday, February 25, 2019

Random thoughts: 5 years after I thought I begin my journey to Rome

This post is a review of a post of investment principles I had 5 years ago in 2014.

https://sillyinvestor.blogspot.com/2014/07/random-thoughts-my-route-to-rome.html?m=1

2014 One paradigm shift:

Stop worrying about the value of my portfolio. Not that it is not important, but the cashflow of dividends and the robustness of underlying business is more important

NOW:

Portfolio value is important. Returns is not as important robustness of portfolio. Keep a decent amount of cash in portfolio. Recent correction with counters in radar falling 50% to 80percent from their historical or recent peak, made me take out my gun and statt firing. The lowest cash went was 40 percent. It is back to 50 percent now with some triming of loses and taking of profits.

Second shift:

Only look at companies with yield of at least 4%. If u expect growth, 4-5% is ok, if u expect flat or zero growth, at least 6% will be appropriate.

NOW: More or less intact the view

Third shift:

Only buy companies that will survive the next downturn and emerge stronger. Trading of companies that are mispriced is permissible with 2 years horizon. Expect such counters to never recover, and be ready to take the risk, and be nimble. Such counters should yield more than 8% to justify the risk.

NOW:

Trading of mispriced counters are about turnaround play. Dividend yield is a redundant marker. The risk reward compensation should be in the form of capital gain and the high yield.that should come only after u are right about the turnaround and dividend Increase to justify the high yield due to the low cost of purchase.

If Its 50_50 kind of turnaround, punt small run fast and accumulate only once.

4th shift:

Do yearly reinvestment of dividends, there is no need to time the market for correction or bear.

NOW: Hahahha, why am I keeping cash if I am not timing the market

5th shift:

Other savings go into cash. Only invest further with new capital injections when cash form more than 40% of portfolio, or

When market correct 10-15 % ( 30% of cash can be a activated )

When market correct 15 - 25% ( up to 60% of cash can be used)

when market correct 30% - 40% ( Up to 100% of cash can be used)

When market correct 40-50% ( cash backs savings from 2 of my endowments plans can be used)

More than 50% ( CPF money can be used )

Keep expanding radar...

NOW:

I go for counter correction too. Of course low tide all boats sink. But if its a industry or company specific correction, I still fire off.

Beside CPF, I have start my maiden investment in SRS. Nope, I am not going to exhuast all cash before using CPF. What good is that.

I will stagger cash and CPF and SRS. So my cash will also get some low prices that allow.me to liquidated at a earlier possible time and not until the next decade.

Radar expanding... but more for interest on business than possible winners.

Random thoughts: What is Real?

The passing by in my life,

Are u real?

I give my best to u, enjoyed your company,

Are we real?

You will be gone in a year or two,

Bringing our laughters, my scolding into memory lanes.

Family ties are real instead, u say.

They are with u all the time.

If time is the test of real,

Then relatively, we are all fake as compared to something more permanent.

An half_life is real,

A winkling flower is real?

We feel it, its real.

Remember that fleeting motivation from that sale talk.

I knew that is not real.

Perhaps, nothing is real.

Is a footprint real?

The footprint seen, felt.

The wish to remember the peeson that man who left behind the footprint.

Long after the wind blow the dusk away,

Is real

Tuesday, February 19, 2019

Random thoughts: How rich am I?

This not a post about net worth, but rather, a compilation of real people I met, and my observations here. I am being judgmental here, so be warned. Names are not real

1) David has a view on how others should leave their lives. Why is the wife Not working, why work as a Expat overseas when the pay is not much higher. Why Not sack the relative at work who is not contributing. Why not looking to buy property.

It will be too late if we dun buy something to leave for our child. We are being passive if we are not striving to grow our wealth actively.

2) Wilson gambles and is in debts. Mountain high of debt. His mum pays off his debt. He ask mum for money evertimes he needs money. Mum sold off property, to stayed with another son while he continue to stay in condo, keep a pet and ask mum for money to pump petrol, and pay for mortages.

Mum in turns ask all her relatives for money. Beg, scold and hoot big big on toto and 4D. She always claim no one care about her. She blows her Hongbao money given as gifts on a single genting trip. Like mother like son. Both are in debts and Wilson is getting marriEd soon with girlfriend already pregnant.

3) Samuel is single. Spend a lot of time giving weekend tuition. Save enough money to buy an investment property. Became interested in stocks. Ask his friend to teach him. His friend who is yours truly silly investor ask how much money can he lose.

Samuel Says 150K. Silly tease him that he is rich as 150K is silly total assets.

Samuel reply is classic:

You have a child that looks like u

You have a wonderful family living together.

You doing well in your career.

You are nice to your family.

You know how to invest.

You are much richer than me.

Silly being silly and failing Maths Agree with Samuel. Although he is no longer doing as well in his career than what Samuel knows, silly never really feel poor.

He knows he might not be as comfortable as others financially, but he doesn't need advice on how to get rich.

He tried to stay away from Wilson and David, and advise others not to be burden by them.

I think I am rich. I think I am happy. U are richer, god bless u. U are happier, cheers. I need no help or words of encouragement or advice from u, Thank you very much

Thursday, February 7, 2019

随心笔:害怕

害怕晚上,

害怕下班后到医院去。

那里环境还不错。

但不知道能为父亲做什么。

虽然,哪里有许多人情况比父亲还糟。

害怕停下来。

害怕思绪乱窜。

过年那几天,害怕呆呆呆在家。

也不知道和“亲戚”说什么。

只提醒自己注意当下,

其他的别想。

回到了学校,

好像是我的救命绳,

逗孩子笑,很开心。

看孩子努力,很欣慰。

很期待每个星期四和篮球队的孩子打十五分钟的球。

我怕,去医院,我也有点怕回家。

今天就在课室外,改簿子,

改了就把簿子分类,放在课室。

其实有更快的方法的。

但是,不知道为什么,知道忙完了,

就要到医院去了,

所以很不积极。

只想留在学校。

看看股票,也闷。

听歌听着听着,

会无厘头地想哭 。

买点什么好,让他止痒。

Saturday, February 2, 2019

随心笔:本来

本来以为都习惯了。

以为没感觉了。

怎么都回来了。

突然想哭。

突然想起以前当义工时,

也是推着老人到公园走走。

说说笑笑。

昨天还教我的学生尽情哭。

把不满都抒发。

我原来也会哭。

本来以为无悔,没什么好哭的。

原来有感觉是这种感觉。

到底是在同情他,还是同情自己。

Saturday, January 19, 2019

随心笔:空屋

我回到了我们的家。

我成长的家。

好像想起你还健康时,

拉着你到外头吃饭的情景。

其实,我知道你很累,

但是不想你一直睡。

走过餐桌,你的药还在药盒。

有时怪你为什么没吃药。

也想起你说肚子饿,

半夜起来橇饼干罐。

现在你在医院,

什么食物都说饱,吃不下。

精神不算太坏,

但是不知道能和你说什么。

就只能按按你的脚,希望你舒服一点。

你在医院三周了,

房子空了三周,

那天回去,赫然发现屋外的植物都快枯死了。

我从很阴郁,到没感觉,

这就是他们说的麻木吧。

空空的,很整齐。

空空的,很平静,不像你刚入院前,

忙得头昏脑胀。

我知道你想快点回家,

不过自私的我,在工人还没来前,

器材还没买前,还是挺赞成医院留着你的。

空屋空屋,过年前能热闹起来吗?

Subscribe to:

Posts (Atom)